#Activism 13. Carrefour Adjusted Leverage Understated

Request for Enhanced Transparency on Financial Metrics

Paris on 30 June 2025

To the members of the Board,

Following the formal transmission of a detailed set of due diligence questions on May 27, 2025 — encompassing more than 200 items across financial risk, franchise litigation, governance oversight, and operational performance — we regret to note that no substantive response has been received to date.

This absence of engagement, particularly in operational matters, raises legitimate concerns about Carrefour group’s openness to constructive dialogue with its shareholders. It also calls into question the company’s current posture regarding transparency, accountability, and the quality of its internal oversight mechanisms.

Such concerns are not isolated. Carrefour group’s financial reporting practices, especially in Brazil, have been subject to scrutiny in the past. As early as 2010, operational and reputational difficulties in the region were publicly documented. More recently, legal actions brought by Promocash franchisees — citing potential informational asymmetries — have further highlighted persistent questions regarding Carrefour group’s disclosure standards.

The recent delisting of Carrefour Brazil reinforces the importance of transparency and reinforces the case for thorough, independent review. Our present analysis has been conducted solely based on publicly available information and reflects a broader assessment of the group’s communication practices, particularly as they relate to financial reporting integrity across its various geographies.

Our review of publicly available financial disclosures suggests a notable discrepancy between Carrefour group’s reported leverage metrics and adjusted figures that account for the impact of factoring and year-end working capital optimization.

While the company reports a consolidated net debt-to-EBITDA ratio of 1.9x, adjustments for financial arrangements not directly supported by underlying cash generation — specifically, over €1.1 billion in factoring operations in Carrefour Brazil and an estimated €360 million benefit from year-end supplier payment deferrals — indicate that actual leverage is materially higher.

On a pro forma basis, incorporating these elements, Carrefour’s group leverage would stand at approximately 2.2x. This adjustment moves Carrefour group away from the profile of a conservative balance sheet and positions Carrefour group among the most leveraged players in the European retail sector, second only to Sainsbury. In Brazil, the divergence is even more pronounced: the reported leverage of 1.3x rises to 2.7x on an adjusted basis — a more than fivefold increase relative to 2019 levels.

In our assessment, the current accounting treatments introduce a disconnect between reported financial metrics and the company’s underlying cash flow generation profile. This divergence may lead to a misrepresentation of the group’s actual leverage and could impair investors’ ability to accurately evaluate the company’s financial risk. These findings also prompt broader questions regarding the consistency and clarity of Carrefour’s financial communication.

Furthermore, the identified discrepancies call into question the Board’s oversight with respect to cash flow quality, capital structure management, and the integrity of financial disclosures. In our view, such matters fall squarely within the scope of sound governance and fiduciary responsibility.

We believe that prompt corrective action is warranted. Carrefour should adopt a more transparent and economically grounded presentation of its balance sheet and reaffirm the standards of financial discipline that have historically underpinned investor confidence in the Carrefour group. The analysis and recommendations that follow are submitted with that objective in mind.

1. Behind the Numbers: Reassessing Carrefour Group and Brazil Leverage

Historically, Carrefour has positioned itself as one of Europe’s most financially disciplined food retailers, consistently maintaining a net debt/EBITDA ratio below 2.0x between 2019 and 2024. As of fiscal year 2024, the company reports group leverage of 1.9x, with its European operations at 2.1x and its Brazilian operations at a notably low 1.3x.

However, a more granular analysis of the Brazilian subsidiary reveals two structural financial practices that materially understate the group’s reported leverage:

Expanded use of factoring: In 2024, factoring activity in Brazil improved reported group net debt by over €1.1 billion, effectively reducing the consolidated leverage ratio by approximately 0.2x.

Year-end trade payables optimization: A recurring fourth-quarter extension of trade payables contributed an estimated €360 million profit to net debt reporting, further lowering leverage by an additional 0.1x.

When adjusted for these two non-cash financial mechanisms - which do not reflect underlying operating cash flow - Carrefour’s group-level net debt increases by approximately €1.5 billion. On this restated basis, leverage in Brazil rises sharply to 2.7x — representing a fivefold increase since 2019, largely attributable to the 2022 acquisition of Grupo Big and the absence of meaningful food inflation in the latter half of 2023 and early 2024.

At the consolidated level, the restated Carrefour group leverage for 2024 reaches 2.2x, exceeding the reported figure by 0.3x. This adjustment repositions Carrefour group from a balance sheet conservative to one of the more levered operators in the European retail sector — second only to Sainsbury.

Carrefour’s group net debt understated by €1.5bn and leverage by 0.3x

Carrefour’s Adjusted Metrics Suggest a Less Conservative Balance Sheet

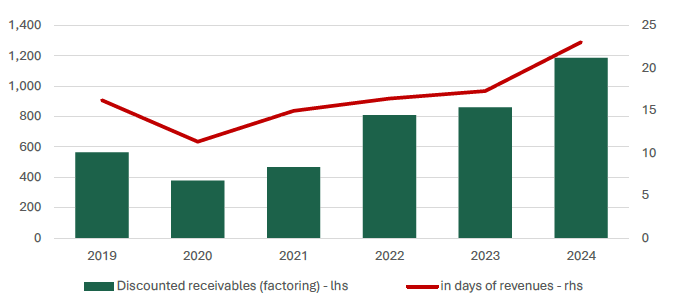

2. Increasing use of factoring in Brazil

Although not explicitly disclosed in Carrefour group’s consolidated financial reports, its Brazilian subsidiary publishes detailed data on factoring volumes. According to publicly available filings, Carrefour Brazil’s reliance on factoring has increased materially over the past five years—from BRL 857 million (€193 million) in 2019 to BRL 6.9 billion (€1.2 billion) in 2024.

This consistent growth reflects both an absolute increase in usage and a rising proportion of revenues being financed through factoring arrangements. While such practices may support working capital flexibility, the scale and acceleration of factoring activity suggest a structural shift in how liquidity is managed within Carrefour group’s Brazilian operations.

The absence of group-level disclosure on this matter limits full visibility for investors and may understate the group’s underlying financial leverage. Greater transparency of the role and magnitude of factoring within the consolidated balance sheet would be beneficial for stakeholders seeking a comprehensive understanding of Carrefour’s group financial risk profile.

Carrefour Brazil’s recourse to factoring (in €m)

3. Systematic year-end working capital optimization via trade payables

Seasonal fluctuations in working capital are a known feature of the food retail sector, reflecting typical inventory buildup and sales cycles. However, the extent of year-end working capital optimization at Carrefour Brazil appears atypical in scale and consistency, particularly as it relates to trade payables.

Since 2019, Carrefour Brazil’s Q4 trade payables have, on average, extended 75 days beyond the Q1–Q3 average, with a 33-day gap still observed in 2024. This suggests a systematic delay in supplier payments of more than a month at year-end, thereby temporarily improving reported net debt levels at the close of the fiscal year.

While such practices are not unprecedented, Casino and GPA have adopted similar approaches during periods of financial pressure, they are not standard across the industry. Notably, peers such as Assaí in Brazil and Ahold Delhaize in Europe and North America maintain more consistent supplier payment terms throughout the year.

Adjusting for a 30-day normalization in trade payables, we estimate that Carrefour Brazil’s 2024 net debt would be approximately €360 million higher. This adjustment casts further doubt on the perception of balance sheet conservatism and underscores the importance of enhanced transparency around working capital management practices.

Carrefour Brazil’s trade payables in days of COGS / WCR in days

Conclusion

In our view, enhanced transparency around factoring practices and working capital management is essential to support an accurate assessment of Carrefour group’s financial position. The growing disconnects between reported financial metrics and underlying economic indicators — particularly in Brazil — combined with the absence of any response to our detailed due diligence inquiries, has raised valid concerns among shareholders regarding the quality of financial disclosure and the Board’s approach to investor engagement.

This lack of responsiveness not only undermines confidence in the company's financial communication but also raises broader governance questions, particularly regarding the effectiveness of Board oversight in safeguarding reporting integrity and maintaining alignment with long-term shareholder interests.

Should these issues remain unresolved, Whitelight Capital is prepared to pursue additional steps within the bounds of constructive shareholder engagement. Our track record reflects this commitment: we have previously taken decisive action, including board-level interventions, in response to material governance deficiencies, most notably in the case of Orpea.

We encourage the Carrefour group to take proactive and structural measures to enhance financial reporting standards and reaffirm the company’s commitment to disciplined capital stewardship. While we remain open to collaborative dialogue, we will act as necessary to uphold transparency, accountability, and long-term value protection for shareholders.

Sincerely, Whitelight Capital

About Whitelight Capital, an investment fund specialized in shareholder social engagement. It is dedicated to long-term value creation by supporting international companies in improving their governance, operational practices and strategic discipline.

Press Contact: communication@whitelight-capital.com

Disclosure of Interest

In accordance with Regulation (EU) No. 596/2014 (MAR) and Delegated Regulation (EU) 2016/958, Whitelight Capital and this founder Kevin Romanteau discloses that it holds only an undisclosed long position in Carrefour S.A. at the time of this publication. This constitutes a direct financial interest in the evolution of Carrefour’s share price. This analysis reflects our opinion based on publicly available data and is intended to promote transparency and financial integrity. Whitelight Capital may adjust its position at any time without prior notice.

Disclaimer

This document contains forward-looking statements, analytical opinions, and investment-related information that involves substantial risks and uncertainties. For full transparency, detailed backup analysis and supporting calculations underlying this assessment are available upon request. Actual results may differ significantly from those anticipated or suggested in this analysis. Our analysis may prove incorrect due to incomplete information, changed circumstances, or analytical errors. Market conditions, regulatory changes, or company-specific developments may materially affect outcomes. Financial metrics and calculations are based on publicly available data that may be subject to revision. This document is provided for informational purposes only and does not constitute investment advice, a recommendation to buy or sell securities, or a solicitation of any kind. Recipients should conduct their own independent analysis and consult with qualified financial advisors before making any investment decisions. Any projections, forecasts, or assessments contained herein are inherently uncertain and may not be realized. Past performance and historical data do not guarantee future results. This document has been produced by Whitelight Capital and external advisors. The information contained herein is based on sources believed reliable but is not guaranteed. Past performance is not indicative of future results.