#Stock 9: Carrefour - Short

Deep Dive - Is Carrefour's Business Model Broken?

Whitelight Capital conducted 6 months deep dives anslysis on Carrefour by interviewing former and current employees and decision makers. WLC published our first concerns 6 months ago, here.

***SHORT THESIS

#Since the ’16, multiple business headwinds have emerged, which appear primarily structural:

Mitigated ‘16-’22 track record: +1.0% revenue CAGR, +4.0% EBIT CAGR, +10% EPS CAGR, amplified by value destruction as in ‘17-’18 restructuration of Dia acquisition in ’14 negatively impacted EPS. Consequently, management stopped investing in the franchising overtaken by large digital corporations. Management decided to rely heavily on store conversion into franchise.

#2016-2022 weakness driven by three primary issues – all fundamentally dysfunctional related:

1) Market share expansion leading to cannibalization effect materialized in revenue per store drop and closings peak

2) Franchise conversion acceleration to transfer Capex in Point of Sale (PoS) to franchisee

3) COGS increased w/ higher supply chain costs/structure costs vs. peers w/ unprofitable model for franchised

Since ’21, Franchisees are contesting Carrefour’s and breaking free to chase high profitability with peer business model. Consequently, many French competitors attract unhappy franchisees.

#Our theory as to why we have seen structural issues – “cyclical or secular issues”?

For decades, large supermarket chains dominated the global food market. But bitter price wars and the growing influence of large digital corporations like Amazon and Alibaba are plunging the sector into crisis.

Food retail in France is less concentrated than places like the UK and Spain where there are fewer players. That means competition is high. Carrefour started to fight market share lost by allocating cash on market expansion – e.g. acquisition DIA in’14 to counter Walmart's offensive. According to Deloitte report, Carrefour ranked from #2 worldwide in 2012 to unclassified in 2023.

Forced to deploy omnichannel strategy, Carrefour is investing a lot in digital, supply chain (warehouse & purchasing center), and less in PoS. The group convert the PoS businesses to franchisee business, bearing the costs to franchisees.

Unprofitable franchisees become rinsed by the Carrefour model on top of imposing unfair contractual conditions vs peer. Unsecure franchised business: Convenience store are cash machine w/ 55% operating profit and 97% are franchised

Business model issues do not appear to abating, more likely to spread:

#Franchised model: Convenience stores, representing 73% of French stores, are the cash machine w/ 55% operating profit and owned at 97% by employees. The increase in legal cases (arbitrage and “procedure de sauvegarde”) raises concerns about business model sustainability and closing stores.

#Provisions: Unfavorable conditions and likelihood (win 90% case) encourage more franchisees to fight in arbitrage. Carrefour provisioned less than €0.70m per store while claims range btw €1m to €15m depending on the size.

#Additional services: Other revenue of €530m invoiced to suppliers seems illegal – already lost two legal suits.

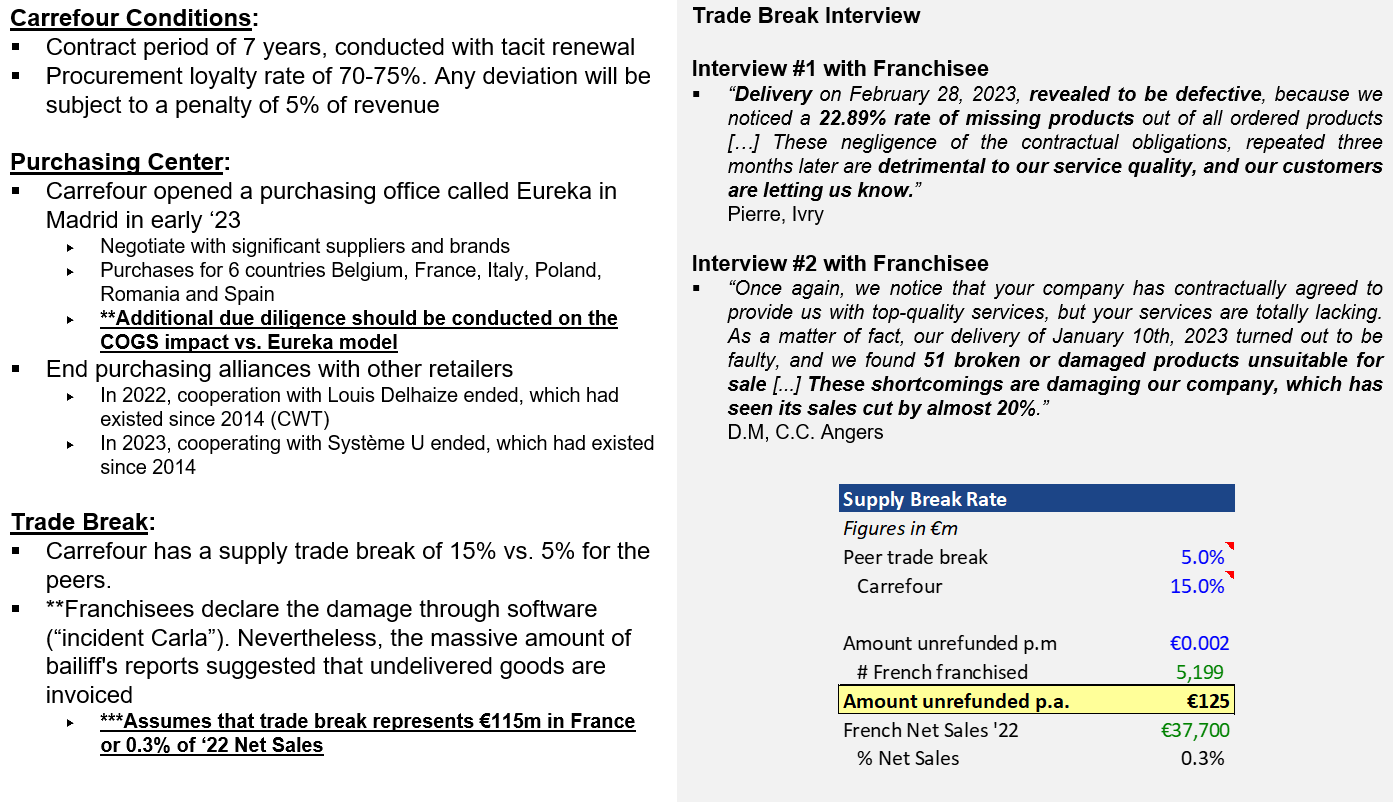

#Supply contract: End purchasing alliances w/ Louis Delhaize and Système U will reduce the bargaining power towards suppliers, putting under pressure COGS. Supply break rate represents 15% vs. 5% for the peer, as such Carrefour poked €115m unrefunded supply.

***CARREFOUR HISTORY

#1963-1992 Modern mass market:

Founded in 1960, Carrefour was led by visionary Entrepreneurs who created the french Food retail leader based on the concept “l’hypermarché à la française” in the surrounding French big cities, inspired by the big American Mall. The Group expanded by acquiring other retail companies (But, Castorama) loved by citizens – And sold it in the late 90’s. The company became listed in 1970.

#1992-2000 Too big to fail:

Mad race of international expansions through 14 countries opened in 5 years, and 3 major M&A acquisitions (Promodès, Comptoir Modernes, Groupe MB), and reached the 4th largest retail Group in the world. In November 1999, Carrefour and Promodès mergerd to face Walmart’s international market share rising and a potential hostile takeover.

#2001-2012 Carrefour focus its strategic shift towards franchise model:

The merger led to 77% shareholder value destruction. Between 1999 and 2012, the share price went from €84.38 to €18.87. In 2008, the entrepreneur Bernard Arnault and Colony Capital entered the capital to restructure the group - and appointed Lars Olofson as the new CEO. In 2010-11, the activist fund Knight Vinke acquired >1% stake in protesting the sale of Dia (hard discount subsidiary - Spanish assets from Promodès) to Blue Capital. In 2012, Georges Plassat was named CEO.

#Since 2012: New management focused on franchising

With G. Plassat (veteran retailer) and A. Bompard, Carrefour stopped to invest in the business / concept, and did only franchisee conversion and M&A acquisition. Since Bompard took the lead in ’17, share price ranged between €13-20

***BUSINESS MODEL

**Unit Economics

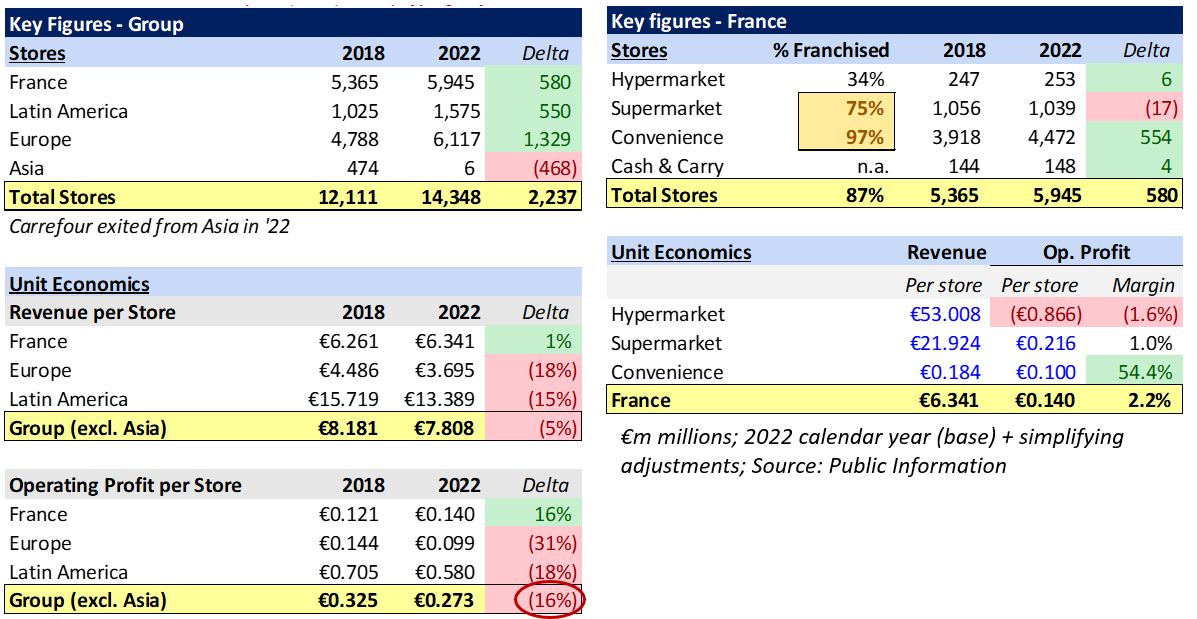

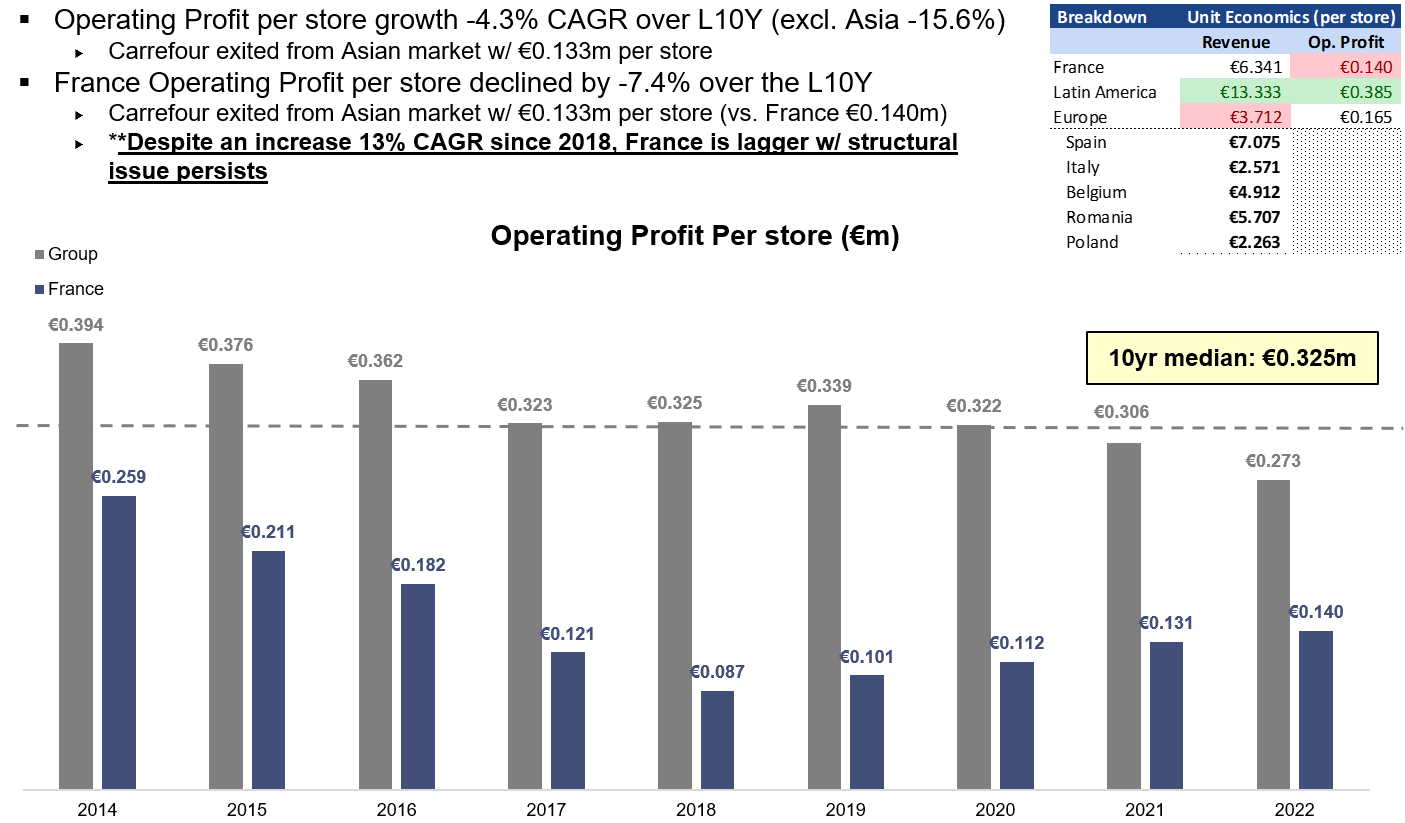

Alexandre Bompard was named CEO at the end of 2017. Over L5Y increased the top line by ~ +1%, and operating profit contracted by -16%. Mgmt. focus on stores expansion at the expense of losing profitability. Exited the Asia market in 2022 mainly due to poor operational performance (Op. profit / store ~ €0.110)

Convenience stores are cash machines w/ ~55% operating profit, offsetting the hypermarket declining model.**Risk: 97% are owned by franchised – unfair conditions and lack of profitability are pushing franchised to shift to peer

**Market Shares

DIA acquisition in ’14 and recent M&A operations increased market share. In Sept-22, announced acquisition of 47 stores in Spain. Nevertheless, this implies a cannibalization effect damaging revenue per store. As a result, Carrefour revenue per store lags peer except in Brazil - Acquired Grupo Big in ’21

**Revenue per Store

**Operating Profit per Store

**Franchise Performance vs. Peer

***FRANCHISED CLAIMS & POTENTIAL LITIGATION

***CLOSING STORES SCENARIOS

***EPS BASELINE

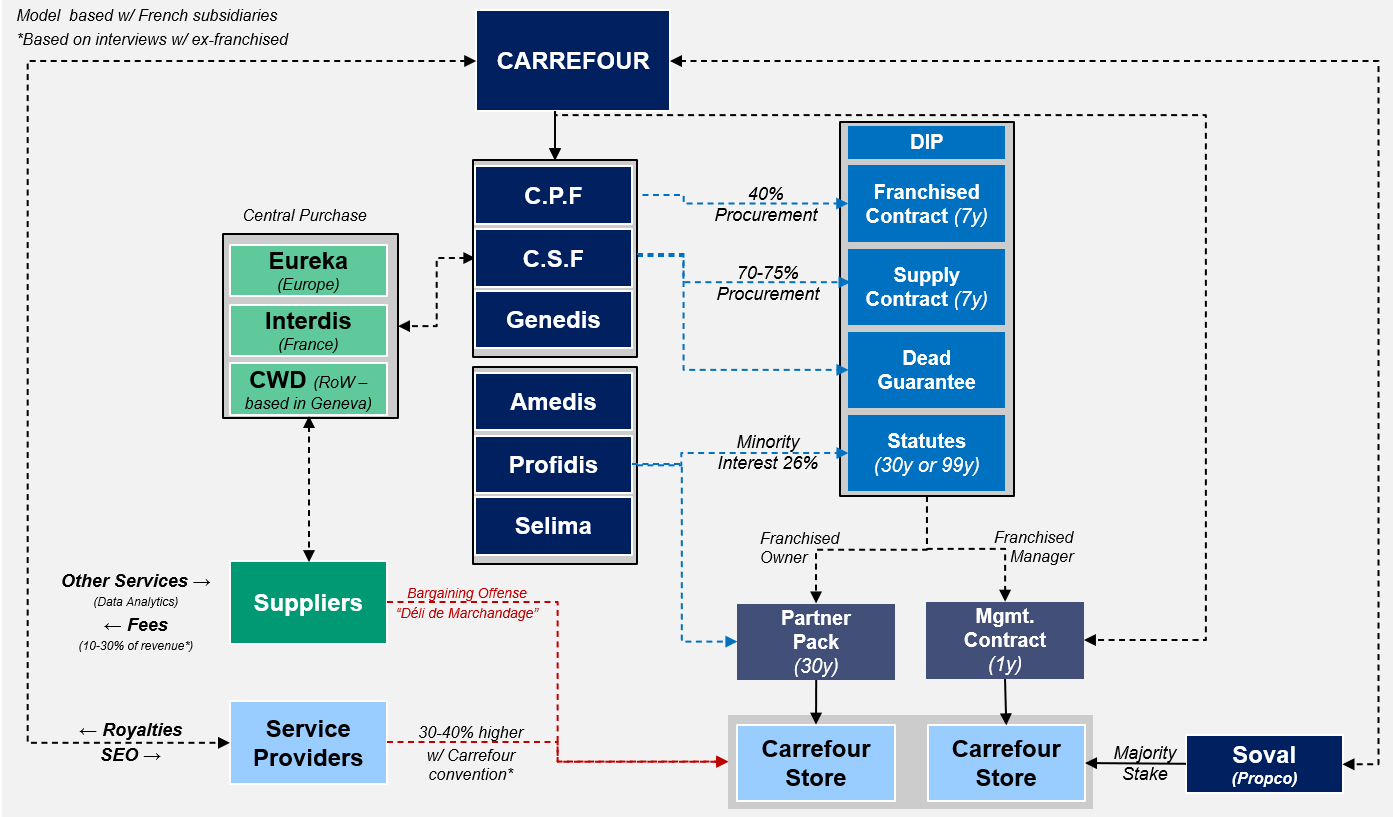

***HIGHLIGHT ON FRANCHISE CONTRACTS

**Pre-contractual Information Contract

**Franchised Contract

**Supply Contract

**Statutes

**Lease Management Contract

**Partner Pack