#Stock 7: Transocean - Long

Deep Dive - 4x1 R/R - Cycle reversion w/ high leverage

***Transocean (RIG)

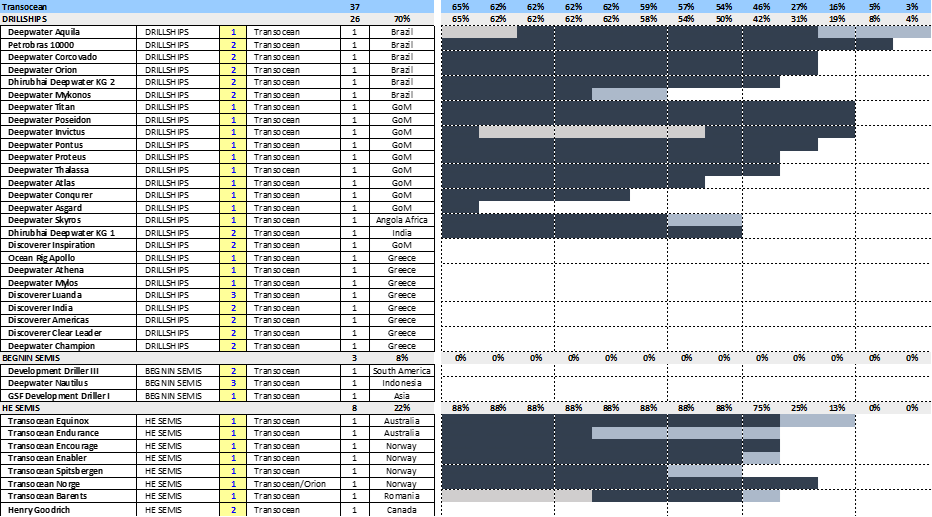

Founded in 1953, RIG is the world’s largest UDW driller w/ 37 floaters incl. 29 drillships (highest specification), and 8 harsh environments (HE) floaters, having streamlined its fleet through the downcycle. Undervalued despite having a strong backlog and highest rigs upgrade.

- w/ revenue US$2,832m in ’23 and EBITDA margin 23.3%

- w/ market cap. of US$4.86bn w/ ADV 3mth ~18.4m and ~16% short interest, EV $US11.9bn incl. US$7.8bn debt, meaning ND/EBITDA 10.9x (4.2x in ‘24E

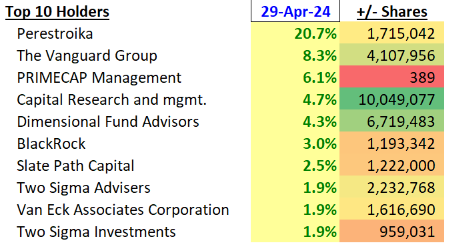

- Main shareholders (float 78%): Perestroika (~21%), Vanguard (8%), PRIMECAP mgmt. (6%)

**Rig Order Book

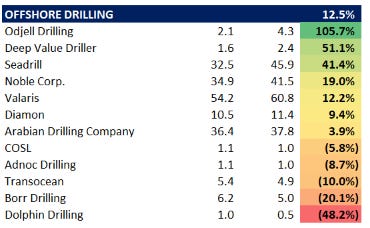

**SP LTM vs. Peers

**Top 10 Shareholders

***Industry

[See our previous sector analysis]

From peak in 2014 to trough2018-19, the offshore rigs market is recovering since 2020.

- In 2020, the activity for floaters was significantly impacted by the COVID-19 pandemic, and the following crash in O&G prices led to a severe drop in global utilization rates and day rates.

- In 2021-’22, after the 7-year downturn, the market experienced a rebound with an increase in activity and improvement in day rates. Rigs that were idle during the downturn started to come back to the market.

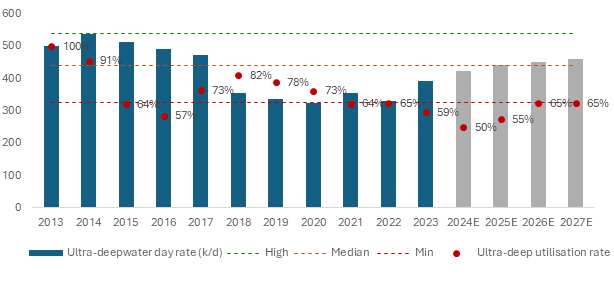

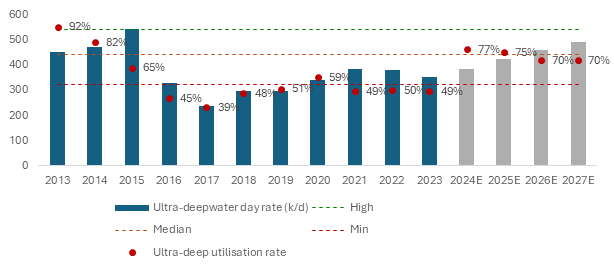

- In 2023-24+, contracted utilization was already in the 90s, with clear visibility for increased demand and no builds in sight. Tailwinds on day rates, which are headed towards $500k/d for both high-end drillships and harsh semis – nearly back to previous 2014 cycle.

-Forward: Rystad anticipates deepwater greenfield CapEx in ‘25 will be the highest in 12 year. By 2027, total deepwster investments will reach nearly US$130bn (+40% vs. ‘23).

**Supply

The offshore drilling industry is highly competitive with currently ~211 floaters in the global market, o/w ~147 are contracted. Reactive of 14 cold stacked drillships will happen if day rate >US$500-500k/d w/ long-term contract. Don’t expect new construction as 7th drillship generation cost ~$600-700m (payback w/ dayrate ~US$550-600k/d).

**Demand

- Norway: The active North Sea fleet is mostly booked for 2024. Equinor is expected to drill 30-34 exploratory wells in 2024, an amount not seen since 2013-15. Considering improving demand in Norway's semisub rig market and other semisub markets such as Namibia, the HE Semisub market is tight and faces a potential shortage in 2025+.

- UK: E&P delayed investment decisions following the windfall tax in May 2022. In Q1 ‘24, the government showed signs of more friendliness to attract more investment from E&P, incl. reduced tax levies and a new licensing round. Floaters demand ~[9-10] floaters (P&A work) vs. total supply [11-12] floaters (incl. Boargland + #2 cold stacked).

- US Gulf of Mexico: The rig supply/demand balance is such that the region could be short 1 rig in 2025. RIG is observing elevated demand from independent operators. There are two major E&P companies currently out to market for multi-year program.

- South America: Brazil accounts for ~15-20% of global floater requirements through 2027 (by duration). The clean dayrate in Brazil remains generally below the global average, but operations have increasing demand MPD and dual capacity (~36% demand in 2024). Brazil could require 36 floaters as soon as 2025. Petrobras may absor up to 30 rigs through 2030. Guyana also contributes to the increase in rig demand. Currently using 5-6 drillships and still only producing $400k bpd vs. $550/600k expected.

- Australia: Plans field with local regulatory agencies and market discussions held indicate that further work will be available for rigs in the region in 2025 and beyond. Dayrates trend towards the higher end or fringes for semisubmersibles, currently ranging between US$225k/d to US$485k/d. Inpex and Chevron’s next phase in their field developments is expected in 2026.

- Namibia & South Africa: demand for higher specification drillships, and deeper projects than Brazil and West Africa. Deepwater HE semisubs have dominated Namibia - higher spec 7G drillers such as Valaris (#2), Eldorado, West Hercules, and Deepsea Bollsta (summer 2024). Total demand estimated ~5-6 rigs.

- Angola and Nigeria: have deepwater growth projects that will also increase rig demand. Transocean and Equinox arrive from Norway in Q1 2024 for multiple contracts, keeping the rig working into 2028 if options are exercised. If demand materializes as currentlu expected, Africa could be the region to absorb most of the remaining available active floating fleet

***Company Fundamentals

- RIG was dubbed “Saudi Arabia of the offshore rig market” for its role in protecting dayrates through stacking rigs in the years post the financial crisis. Very well disciplined through this cycle both by keeping rigs out of the market, and by pushing drillship rates.

- Experienced management w/ strong capabilities execution to position rigs in strategic location.

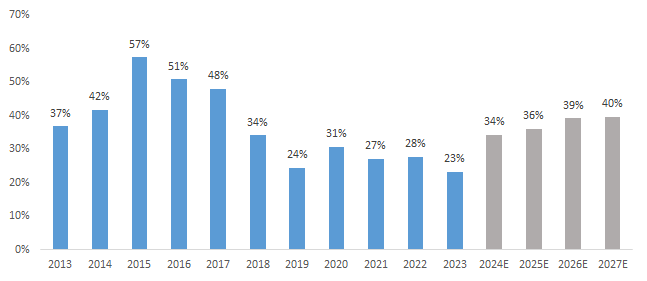

- As the only large floater company not to restructure in the aftermath of the pandemic, RIG remains highly leveraged compared to peers w/ ~65% of EV.

- Previous ’14 peak, EBITDA per rig ~ US$40-50d/k vs US$33k/d, mostly impacted by reactivation costs and operating expenses ~65-70% of sales vs. ~40% in 2014.

***Thesis Points

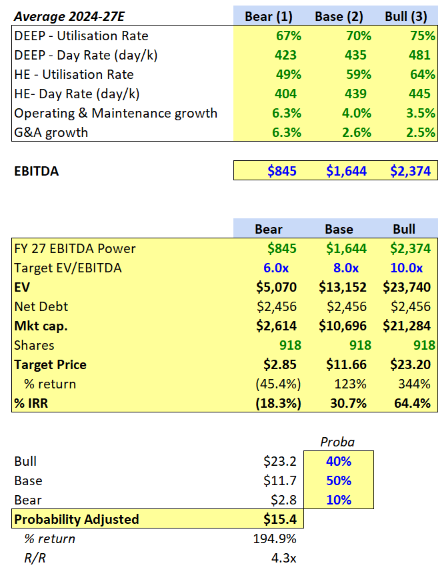

#1. Day Rates: Day rate surges from ~US$300k/d to US$500k/d in 3Y - contract getting longer as market tightens. We assume avg. dayrate ~US$440k/day N3Y (=avg. L10Y / ’14 peak ~US$530k/d).

**UDW Dayrate

**HE Dayrate

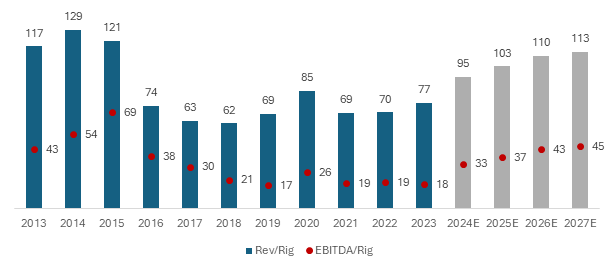

#2. Revenue Growth: We assume the reactivation/contract of 5/6 rigs with an overall 66% utilisation rate (< 2014 peak level), supported by high oil prices above US$80bpd and E&P capex.

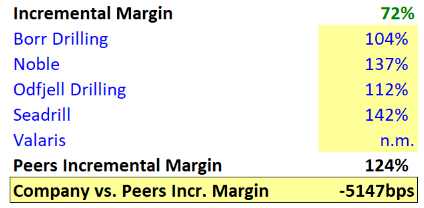

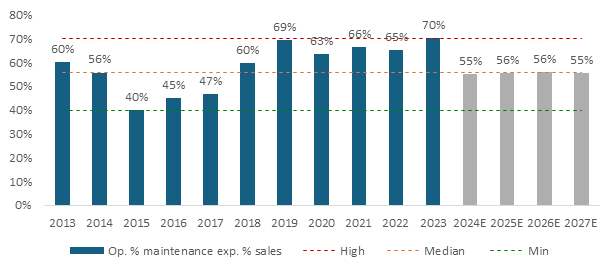

#3. Incremental Margin: Improvement in incremental margin ~70% over N3Y due to cost reduction in reactivation (maintenance ~60-70% of sales btw ‘19-23) and operating leverage effect. We assume EBITDA margin ~40% (EBITDA per rig ~$45m in ‘27), near to ’14 peak level.

**Incremental Margin N3Y

**Unit Economics

***Risk Points

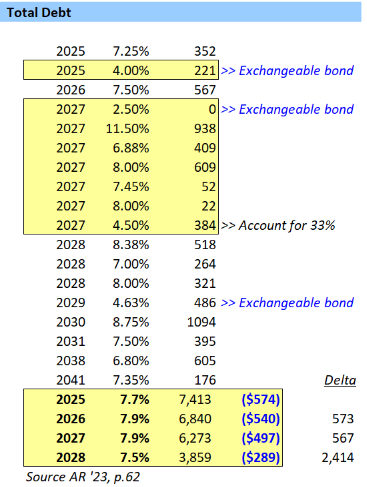

#1 Risk. Debt burden: RIG has ND/EBITDA ’23 ~10.4x. Most debt are maturing (~50%) btw 2026-27 incl. 33% in 2027. Mitigants: highest utilization rate vs. peers over N3Y, which will allow smooth deleverage w/ ND/EBITDA ~4.2x in ’24 and 3.4x in ’25. Moody’s upgraded RIG rating to B3 from Caa1.

**Debt Maturity

#2 Risk. Available capacity: According to Barclays, of the 67 contracted 7th/6th gen drillships industrywide, 15 come off contract in 2024 (inc. 3 in 2Q) with two currently idle. Mitigates: RIGS has a favourable backlog with most contract coming off at the end of 2026.

***Valuation starting point & 3-year algorithm

- RIG is currently trading at premium 7.7x NTM EV/EBITDA vs. 6.8X peers. Negative investor sentiments toward w/ FCF allocation and mis-exxecution in Q1 ‘24, missing earnings. Compared to street, we think that RIG premium is justifyed due to the fleet high specification vs. peers and strong track record.

- In our base case scenario, we expect the company to have a 3-yeatr CAGR revenue growth of ~15% organic assuming ultra-deep avg. day rate 445k/d and avg. utilisation rate 73%, HE avg. day rate 440k/d and avg. utilisation rate 59%; 40% EBITDA margin and ~70% incremental margin (vs. +125% peers).

***Estimates vs. Street

- Trading path: Some catalysts that is 6-18 months away – too long for impatient market.

o AGM on 16-May-24 AGM / 2Q’24 on 29-Jul-24 / feet status 7th generation reactivation

- We expect in’24 US$1,580m EBITDA (US$45 per rig) vs. US$1,240 (US$35 per rig) from street, FCF yield 8-10% vs. 5% from street.

***Upside, Downside, Risk/Reward

RIG is trading at US$5.87, trading 52-weeks high -37% and +26% low.

3-year reward case is +195% and 12-month risk case of -45% for a nearly meaning 4x1 R/R.

***Appendix 1. Share Price

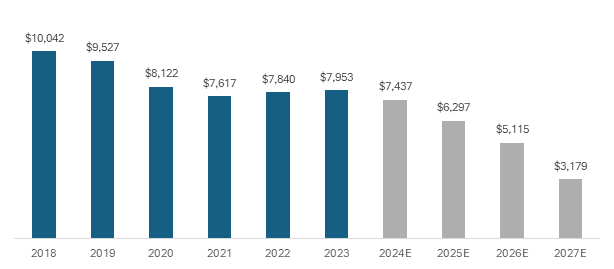

Appendix 2. Operating & Maintenance expenses

Appendix 3. EBITDA Margin

Appendix 4. FCF per Share

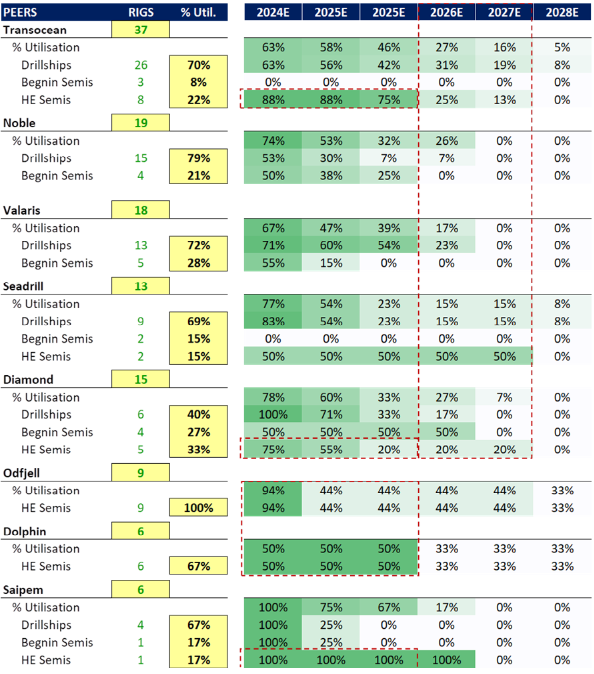

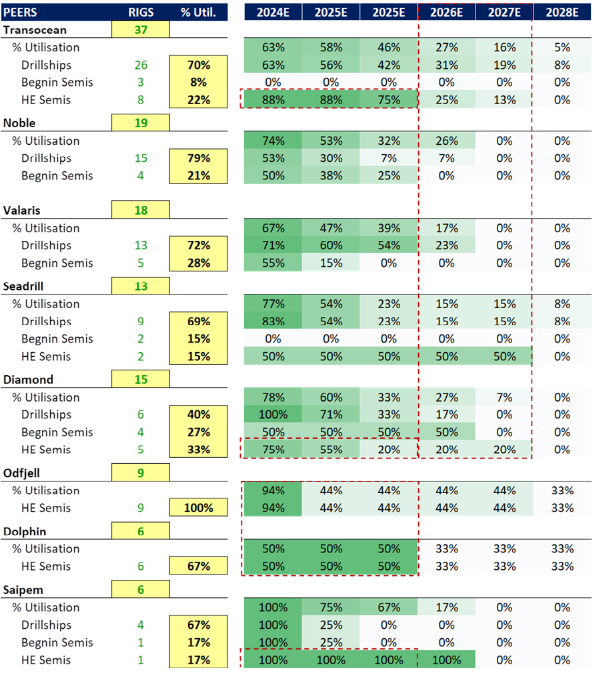

Appendix 5. RIG Higher Utilization vs. Peers

$RIG MAY recap

1) 25% post earning run

2) PBR new Chief says moar offshore

3) Elliott buys $9.7mm

4) Insider buys $12mm

5) $SDRL merger rumor

6) Added to Russell 2000 Value Index

+positive market dynamics & all

interested on thoughts on RIG after Monday 3rd. I've held off on buying until now. A thesis I have is that we are going to see long term bifurcation in the offshore rig market, and the low spec and even 6G drillships are going to have lots of supply white space.

This is great because RIG at 4 is pretty much the only offshore driller that gives you exposure to the thesis now. But probably burns alot of the sector beta / TV assumptions people previously priced in.

if your interested, dm me. I have a day-rate quantitative forecast to prove point 1 above.