#Stock 6: Eramet - Long

Quick Dive / Perf +40% since our intial position in Oct-23 / Beach ball trade!

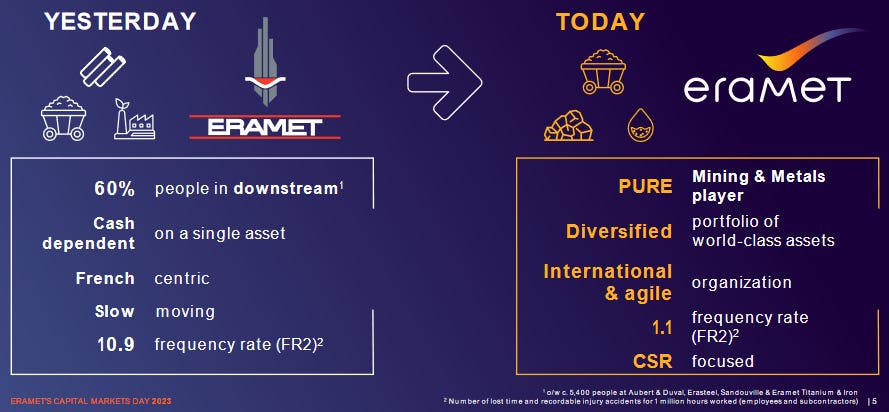

***Eramet Overview

• Leader player in the mining industry historically positioned on the manganese ore & alloys, nickel and mineral sands

• High quality strategic assets through 5 mining sites and 3x processing plants – well-positioned for the energy transition

- Africa (2x): Manganese mine in Gabon + Zircon/Titanium in Senegal

- Asia/Oceania (2x): Nickel + Cobalt mine in New Caledonia + Indonesia named Weda Bay (only Nickel)

- Argentina (1x): Lithium plant – portfolio expansion w/ production start in Q2 ’24

- Processing plants (3x) based in the US, France, and Norway

• EBITDA split geo ~40% Gabon, 30%OECD, 18% Indonesia, 9% Senegal, 4% New Caledonia

• Mkt cap: €2.2bn w/ ADV: 56k, Beta 1.5x / EV €3.1bn incl. ND €0.6bn / EV/EBITDA NTM 4.8x / Div. yield 4.8%

• Current SP trading at €73 - peak to €160 in H1 ’22 since then range btw 60-100

• Shareholders: Duval Family 37%, French State (APE) 27%, [STCPI 4%], Free Float 32%

***Manganese (~60% sales)

• #1 producer of manganese worldwide w/ 7.5Mt of ore produced in ’23

• Owing 25% of the world’s management reserves, w/ mining plant in Gabon (Monada)

• Moanda had a high-grade ore asset with a pricing premium (#2 player after GEMCO, Australia)

• Produced 365 kt of manganese alloys in 2023 – Note that Gabon mine is the main cash co when Nickel is tough

• Revenue FY23 ~€2.0bn sales declined by -37% yoy vs. CAGR +12-13% over L5Y – back to pre-covid level

• EBITDA margin at trough w/ 25% margin vs. 37% over L5Y

• Drivers: 90% carbon steel industry (50-70% construction / 10% automotive), 10% other industries

• Main competitors South 32 (spin-off of BHP in 2015)

***Nickel (~30% sales)

• Largest nickel mine in the world named Weda Bay in Indonesia – named SNL

• Owns 38.7% stake alongside Tsingshan, the majority shareholder (51.3%), and the Indonesian government (10%)

• Revenue FY23 ~€1.0bn, -29% yoy vs. CAGR 17% over N5Y – back to 2020-level

• EBITDA -€120m, nickel plant runs impacted reduced output after power incident

• Drivers: Main nickel application: 66% stainless steel, 15% batteries – China strong driver of growth

• Valuation implied EV/EBITDA ~4.1x – reverse DCF rev. growth -5% until 2033 and then flat / EBITDA margin 40%

• Expectations: Street target price ~€80 assume zero value for SNL / mkt growth 12% p.a. until 2030

• Market sentiments: SNL is the main concern due to cash burn, exiting would be the best option (politically difficult)

• Glencore stopped financing loss making nickel site in Q3 ’23 (49% stake) in Koniambo – article / exited in Feb-24

• Rumour potential partnership btw France and Australia to support Nickel production – recent government visit on the ground

***Mineral Sands (~10% sales)

• Entered the space in 2019 – production seems to decline and limited growth till ’26 w/ mkt shares 11% ‘26E

• Produce Zircon very niche market w/ 2/3 players – output used in nuclear production • Revenue declines -12% yoy, usually growth ~30% since ’19 (except -4% in ’20)

• Drivers Zircon: 50% ceramics, 20% chemical, 30% refractories & foundry

***Lithium (ramp-up production)

• Strategic into Lithium production in Argentina – start production in 2024

• Produce target ~24 kt annual lithium / 10MT Carbone Equivalent mineral resources

• Full ramp up in ’25 - Sales ~ €100m in ’24, ~€340m in ’25E and €826m in ‘26E

• Normalized EBITDA margin is expected to shift from 40% in ’24 to 73-74% in ‘26

• Seems to have a competitive advantage w/ advanced technology (to be check)

• Cash cost production ~4.5/5k (mgmt) vs. 13.6k – below peers (see charts below)

• Expectation: little bit skeptical/concerns w/ oversupply capacity destroying S&D balance vs. street

• Mgmt growth forecast +20% p.a. until 2030